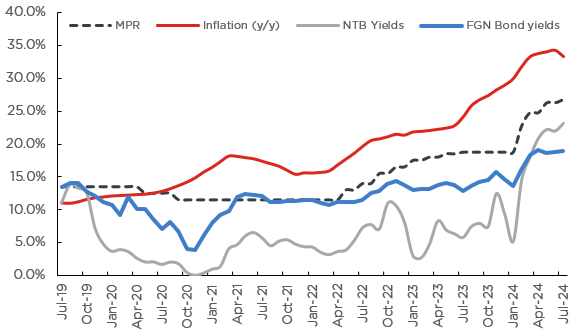

The Monetary Policy Committee (MPC) of the Central Bank of Nigeria (CBN) voted to increase the Monetary Policy Rate (MPR) further by 50bps to 26.75% (Previous: 26.25%) at its July policy meeting. The Committee’s decision to raise the policy rate was hinged on their goal to ensure price stability, given the persistent increase in inflationary pressures. Notably, we point out that the MPC’s interest rate hike is the slowest increase this year, primarily due to an anticipated disinflation trend in the near term. Additionally, the MPC tightened the asymmetric corridor around the MPR to +500bps/-100bps (Previous: +100bps/-300bps) while holding other parameters constant – the Cash Reserve Requirement (CRR) for Deposit Money Banks (DMBs) and Merchants Banks at 45.0% and 14.0% respectively, and the liquidity ratio at 30.0%.

On Domestic Growth: The MPC acknowledged the slow but positive growth in the GDP in Q1-24 (2.98% y/y vs Q4-23: 3.46% y/y), mainly driven by moderate growth in the oil and non-oil sectors. Nonetheless, the Committee upheld its GDP forecast of 3.38% y/y for 2024E, slightly above the reviewed IMF forecast of 3.1% y/y but below the Federal Government’s projection of 3.88% y/y.

On Inflation: The Committee noted the rise in inflationary pressures to 34.19% y/y in June (May: 33.95% y/y), primarily driven by exchange rate pass-through, higher food prices and energy and transportation costs. Additionally, the Committee acknowledged the FG’s effort to increase food supplies and slow down prices following the recently implemented 150-day import duty-free for some imported food commodities as well as the distribution of fertilizers to boost agricultural output. Notably, the Committee stated their expectation for disinflation in the coming months as the tight monetary policy continues to slow down the demand-pull factors driving inflation.

On Foreign Exchange: The MPC noted the narrowing gap between exchange rates across different market segments, signaling better price discovery and enhanced market efficiency, thus limiting arbitrage and speculative activities. Furthermore, the Committee commended the CBN’s efforts to strengthen the FX reserves while encouraging the institution to maintain initiatives to boost inflows, especially through diaspora remittances to build market confidence and support the stability of the naira. Additionally, the Committee recognized the increased efforts by the Federal Government and the private sector to increase domestic refining capacity, which is expected to lower the demand for foreign exchange needed for importing refined petroleum products.

Cordros’ View

Before the meeting, we stated that the MPC would maintain their tight monetary policy stance on four key premises – (1) ensure price stability, (2) reduce the negative real rate of return, (3) manage inflation expectations, and (4) stabilize the naira. Thus, we argued for a 100bps hike in MPR. Although our direction for further tightening of monetary policy was accurate, the Committee voted to raise the MPR less than we projected by 50bps, pushing the MPR to 26.75% (previous: 26.25%). While the modest rate increase primarily reflects their anticipation of moderating inflationary pressures in the near term, we believe their directive was also swayed by concerns over escalating borrowing costs for both the government and corporations following the previous aggressive rate hikes. Additionally, the MPC’s decision to narrow the asymmetric corridor around the MPR to +500bps/-100bps (previous: +100bps/-300bps) appears to be driven by its move to further tighten monetary conditions without significantly raising the policy rate.

Furthermore, the MPC highlighted that the still tight financial conditions in the global economy and the ongoing geopolitical tensions continue to pose an upside risk to domestic inflation. Nonetheless, the Committee pointed out that whilst they expect global inflation to continue moderating, it will remain significantly above set targets, forcing central banks, especially in advanced economies, to keep interest rates elevated. Therefore, the Committee expects global financial conditions to remain tight through 2024 and 2025. Whilst the MPC’s view on a sustained disinflationary trend aligns with ours, we highlight that inflation is settling within target in the UK and approaching target level in the US and the Euro area. Whilst the European Central Bank (ECB) began lowering interest rates in June, we anticipate the Bank of England (BoE) and the US Fed will initiate their first rate cut at their respective September monetary policy meetings.

In the domestic economy, as stated in our June 2024 CPI report, we posit that inflation may have peaked in June and should start to moderate in July as the price shock from the subsidy removal and the currency devaluation in June 2023 begins to fade. In this vein, we expect the MPC to lean towards a neutral monetary policy stance, that is, a wait-and-see approach, in its next monetary policy meeting in September, allowing the impact of previous rate increases to permeate the economy. Additionally, the surge in the government’s borrowing cost following the uptick in fixed income yields is expected to underpin the MPC’s decision to pause its policy rate hikes. Consequently, we expect the MPC to “HOLD” the MPR and other parameters constant at their meeting on the 23 and 24 September.

Market Impact

Fixed Income: In recent weeks, yields in the fixed income market have maintained an upward trend. Specifically, the average yield for longer-term securities has risen to 19.20% as of 23 July (June: 18.75%). Concurrently, the average stop rate at the bond auction yesterday (22 July) increased by 52bps to 20.96% (June: 20.44%). Against this backdrop, we expect the MPC’s recent rate hike to drive further increases in fixed income yields, as investors seek better returns. However, this rate hike may also lead to more cautious investors’ sentiment, as market participants monitor economic conditions and monetary policy closely. We anticipate that the NTB auction scheduled for tomorrow will provide further clarity on the direction of yields in the secondary market.

Equities: Before the meeting, we noticed that the increase in yields in the fixed-income market reduced interest in equities, particularly among domestic institutional investors. While the smaller increase in the MPR may suggest a more moderate approach to monetary tightening, we do not anticipate a significant shift in the market’s trading pattern. In the short term, we expect the full commencement of the HY-24 earnings season to dictate market performance. Subsequently, as domestic investors remain the dominant players in the market, (65.0% market share as of May), we believe sensitivity to rising fixed income yields will remain a downside to market performance in the medium term.

Cordros

Trend in Monetary Policy Rate, Inflation, and Bond Yields

Sources: CBN, NBS, FMDQ, Cordros Research